Credit Default Swaps Explained And Why They Still Matter Today

Last updated: Oct 7, 2022

Credit default swaps made headlines in the 2008 financial crisis. It's good to know how it works. And the problems it can still cause today.

Credit default swaps made headlines in the 2008 financial crisis. It's good to know how it works. And the problems it can still cause today.

What Are Credit Default Swaps (CDS)?

A bank sometimes loans a sum of money to someone as a bond. The bond won't work if the bank is unable to pay. So you can get insurance from a 3rd party, so if the bank can't pay, the 3rd party will.

You will still get paid because a 3rd party has promised you they will pay if the bank can't.

So, CDS is debt insurance.

CDS costs money, and you pay a premium for the insurance. Like you would do on any other insurance.

The Role of CDS in The 2008 Financial Crisis

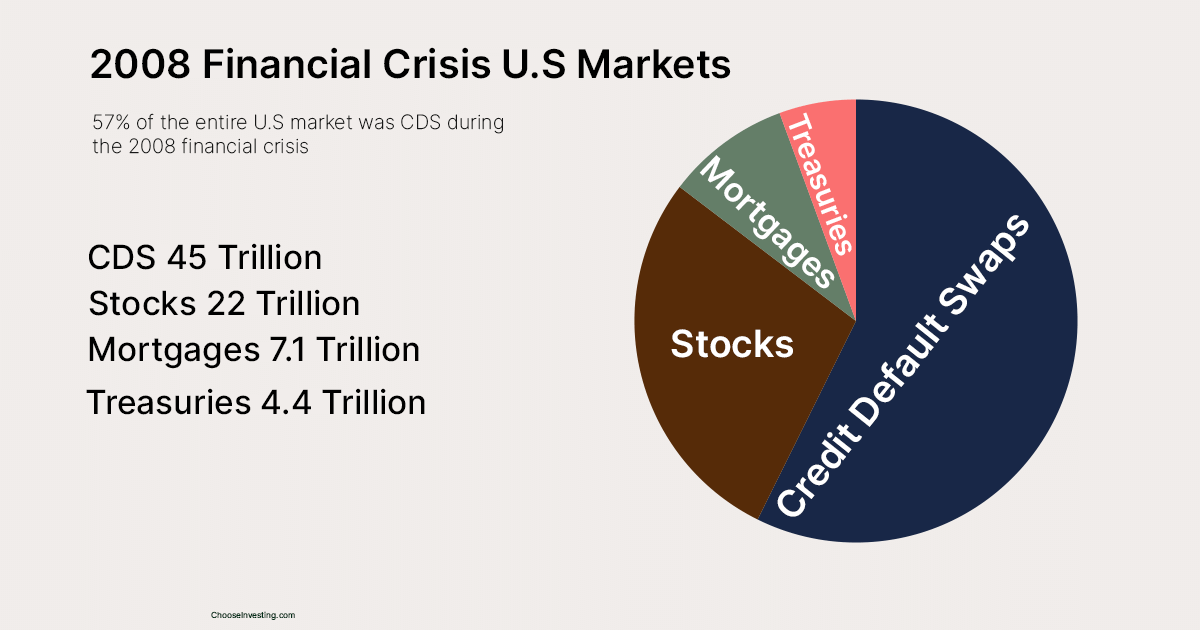

The problem was that every bank used CDS. And it was more valuated than the entire stock market, mortgages, and U.S treasuries combined.

The issuers of CDS didn't have to do anything and still received the premium from it. They didn't set aside the money that they got paid to guarantee. Or do anything, so enough banks and insurance companies thought this was free money.

They didn't issue a CDS for a bond or two but as many as possible. Since when do banks go bankrupt. And who the hell doesn't pay their mortgages? Free money, yes, please!

When the first bank failed, it started a domino effect that had to stop. So the Federal Reserve stepped in and bailed out a few banks.

When enough hedged risks get unhedged, it's a problem. You paid to hedge these bonds, and it didn't happen.

CDS has become more regulated since then. A bank could sell insurance more than ten times its capital without regulation.

It was a reality during and before the 2008 financial crisis.

Why CDS Matters Today

If a large bank goes bankrupt, it's a problem for the entire global economy. Investors don't trust the bank if the CDS price costs too much.

And then these banks could have more difficulties raising money. Banks need to borrow money to fund their business. A bank is a borrower that borrows money.

And if CDS costs too much, it's also a signal. The seller believes there's a greater risk of default on the debt.

There are more regulators today, but CDS still exists and matters. And those regulators may not be enough since they still cause problems.

Sometimes the people in charge of a bank take out money from the company in the form of high salaries. So if your bank fails, it's still very profitable for you.

The U.S has a 5-year average of 21.5, and Russia has 13775. Meaning the probability of default is many times higher in Russia today. Or at least that is what the CDS sellers think.